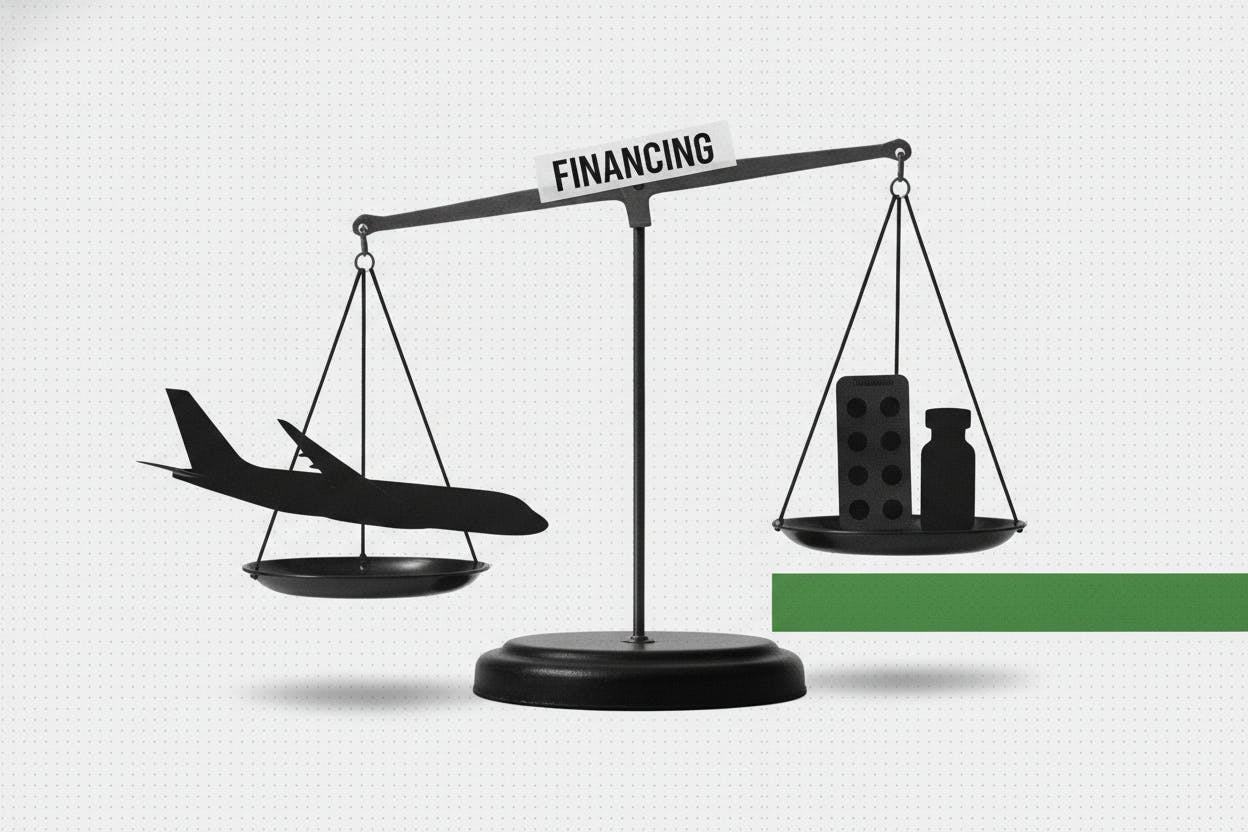

Apollo Global Management, one of the world's largest private-equity firms, has made two big moves that highlight its strategy of chasing both cyclical and steady returns. The firm put $7.65 billion on the table for UK airline EasyJet and agreed to invest €3 billion for a minority stake in a newly created company holding Bayer's long-acting reversible contraceptives business.

The EasyJet bid comes after Apollo previously offered £5.7 billion for the airline, a deal that disrupted EasyJet's existing arrangement with Castlelake. The new $7.65 billion offer represents a significant increase, reflecting Apollo's confidence in travel demand despite economic uncertainty. The Bayer deal, meanwhile, gives Apollo a foothold in a healthcare segment where sales tend to be more predictable, as contraceptives are a recurring need for consumers.

Why Two Very Different Deals?

Private-equity firms like Apollo often rely on borrowed money to fund their acquisitions. Lenders are generally more comfortable offering cheaper, longer-lasting loans to businesses with dependable cash flows, while volatile companies like airlines face higher financing costs and stricter loan terms. With the 10-year US Treasury yield hovering around 4.57%, the cost of debt is a critical factor in how much return Apollo can generate from each deal.

The EasyJet bid is a bet on travel demand and pricing power, which can swing with fuel costs, consumer spending, and the broader economy. Airlines are classic cyclical businesses: they boom when the economy is strong and struggle when it weakens. Apollo's offer suggests it sees value in EasyJet's network and brand, but the deal carries more risk than a healthcare investment.

The Bayer deal, by contrast, is a carve-out of a stable revenue stream. Contraceptives are a mature market with steady demand, and Bayer's long-acting reversible contraceptives (like intrauterine devices) have a loyal customer base. By taking a minority stake, Apollo gets exposure to predictable cash flows without taking full control of the business.

What It Means for Apollo's Investors

Investors typically judge a private-equity firm's pipeline by how bankable each deal is. A healthcare carve-out with recurring demand can support more predictable borrowing and, in turn, more stable fee income and performance pay for the manager over time. An airline deal is usually the opposite: cash flows can lurch with the cycle, so the numbers can change quickly when interest rates or credit conditions shift.

That's why moves like these can influence how investors think about Apollo's future deal profits, especially when longer-term rates are still relatively high. The mix of a cyclical airline bid and a steady healthcare investment gives Apollo a diversified portfolio, but it also means the firm is exposed to different risks. If the economy slows, EasyJet's earnings could drop, while Bayer's contraceptives business would likely hold up better.

For context, other private-equity firms have been active in healthcare deals recently. Warburg Pincus and ADIA are nearing a $7 billion deal for rare-disease pharmacy PANTHERx, showing that steady healthcare cash flows remain attractive to investors. Apollo's Bayer investment fits a similar pattern.

Broader Market Context

The deal activity comes as markets are relatively calm, but investors are rotating out of tech stocks and into other sectors. The US equity funds saw $25 billion in inflows recently as AI optimism returned, but the broader market is still adjusting to higher interest rates. Apollo's ability to finance these deals will depend on credit conditions, and the 10-year Treasury yield at 4.57% means borrowing costs are not cheap.

EasyJet's shares surged on the deal news, along with Vodafone, as geopolitical worries capped gains on the FTSE. The airline's stock price reflects investor optimism that a bidding war could emerge, but Apollo's bid is already a significant premium to EasyJet's previous trading levels.

What Investors Should Watch

For everyday investors, the key takeaway is that Apollo is balancing risk and reward. The EasyJet bid is a high-stakes bet on travel, while the Bayer deal is a more conservative play. How these deals unfold will give clues about the health of the private-equity market and the broader economy.

If Apollo can secure financing for both deals on favorable terms, it could signal that lenders are still willing to back leveraged buyouts despite higher rates. If the EasyJet bid falls through or faces regulatory hurdles, it would highlight the challenges of doing big deals in a volatile environment.

Either way, Apollo's dual moves show that private-equity firms are still hunting for opportunities, even as the cost of capital remains elevated. For investors, watching how these deals progress can provide insights into where the market is heading.