India's Shapoorji Pallonji (SP) Group has finally closed a refinancing that had been in the works for months, accepting bids for 215 billion rupees ($2.25 billion) in three-year zero-coupon bonds. The bonds carry a yield of 18.95% and are secured against the group's stake in Tata Sons, the holding company of the Tata conglomerate.

The deal, reported by Reuters, marks a critical step for SP Group, which has long sought to unlock value from its roughly 18.4% holding in Tata Sons—the largest minority stake in the company. The bonds were issued through Eqyizen Investment and are backed by shares held via Cyrus Investments. Most of the proceeds will be used to replace existing debt, according to sources familiar with the matter.

How the financing works

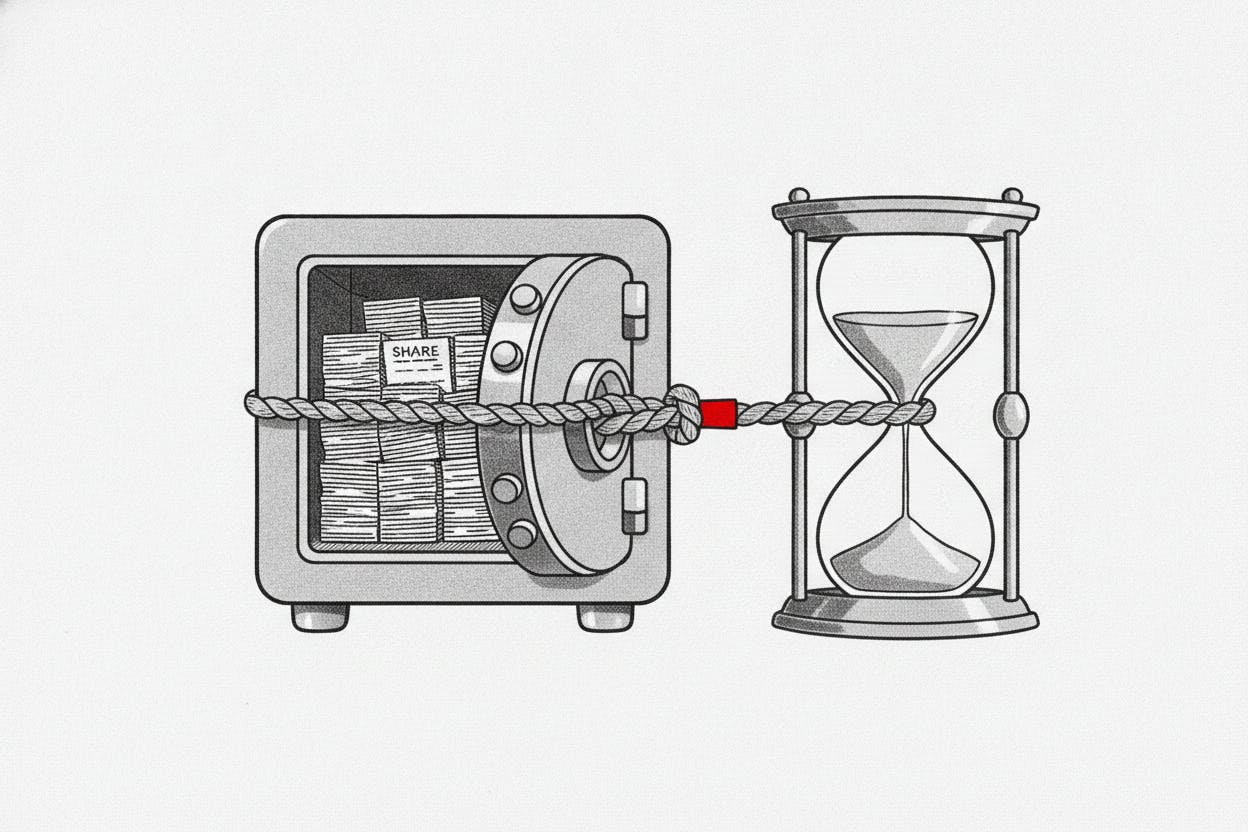

Zero-coupon bonds do not make regular interest payments. Instead, the interest accrues over the life of the bond and is paid in a single lump sum at maturity. In this case, the 18.95% yield means the amount owed will grow each month, and the full principal plus accumulated interest comes due in one "bullet" payment after three years.

Investors were told that SP Group plans to monetize part of its Tata Sons stake within 18 months, either through a listing or a share sale. That timeline is crucial because the longer the group holds the stake, the larger the final repayment becomes. If the monetization is delayed, lenders could face a much bigger cash call or be forced into extension talks.

Some of the demand for the rupee bonds came through Mercury Finance, a Mauritius-based vehicle that raised $650 million in three-year dollar bonds at a 14.50% yield. According to one source, those proceeds were funneled into the rupee issue alongside private credit funds. The near-19% yield reflects the high risk of this kind of financing—lenders are being compensated for both credit risk and the possibility that the exit timeline slips.

What it means for investors

For everyday investors, this deal highlights the risks and rewards of high-yield, equity-backed financing in India. The 18.95% yield is well above what you'd get from typical corporate bonds or government securities, but it comes with significant uncertainty. The entire repayment hinges on SP Group's ability to sell or list part of its Tata Sons stake within 18 months. If that doesn't happen, the debt could be extended, and the final payment would be even larger.

This type of promoter or holding-company borrowing secured on strategic equity stakes tends to come with tougher lender protections—tighter covenants and bigger valuation haircuts on the collateral—than a plain corporate bond. Investors in these bonds are essentially betting that SP Group can execute its monetization plan on time.

The broader context matters too. India's bond market has seen a flurry of activity recently, with the government auctioning 320 billion rupees of bonds and the Reserve Bank of India tightening rules on derivatives trading. High-yield deals like this one are relatively rare and often signal that the borrower has limited alternatives. For comparison, the India bond auction earlier this week tested market demand for safer government paper, while the RBI's funding curbs have slowed derivatives trading, pushing some investors toward alternative assets.

Why the timing matters

SP Group's refinancing comes at a time when Indian markets are navigating mixed signals. The Nifty 50 has edged higher recently, lifted by IT and banking stocks, but the rupee is under pressure near record lows due to oil costs and dollar demand. Gold discounts have widened in India as buyers hold out, while China premiums remain steady. These crosscurrents make high-yield, collateral-backed deals like this one a test of investor appetite for risk.

For SP Group, the deal buys time but doesn't solve the fundamental challenge: turning a large, illiquid stake in a private company into cash. The 18-month plan to list or sell part of the Tata Sons stake is ambitious, and any delay could force the group back to the market for another refinancing—likely at even higher rates.

Investors watching this story should keep an eye on Tata Sons' own plans. A listing of Tata Sons, which has been speculated for years, would be a game-changer for SP Group's ability to monetize its stake. Until then, the high-yield bond market will be the group's primary lifeline, and the 18.95% yield is a reminder that lenders are being paid handsomely for the risk.