Getty Images Holdings (GETY) has seen its stock tumble roughly 44% over the past twelve months, as the visual content company wrestles with two major headwinds: a proposed merger with rival Shutterstock that is drawing regulatory scrutiny, and a debt burden that has climbed to nearly ten times its annual earnings before interest, taxes, depreciation, and amortization (EBITDA).

What's behind the stock slide

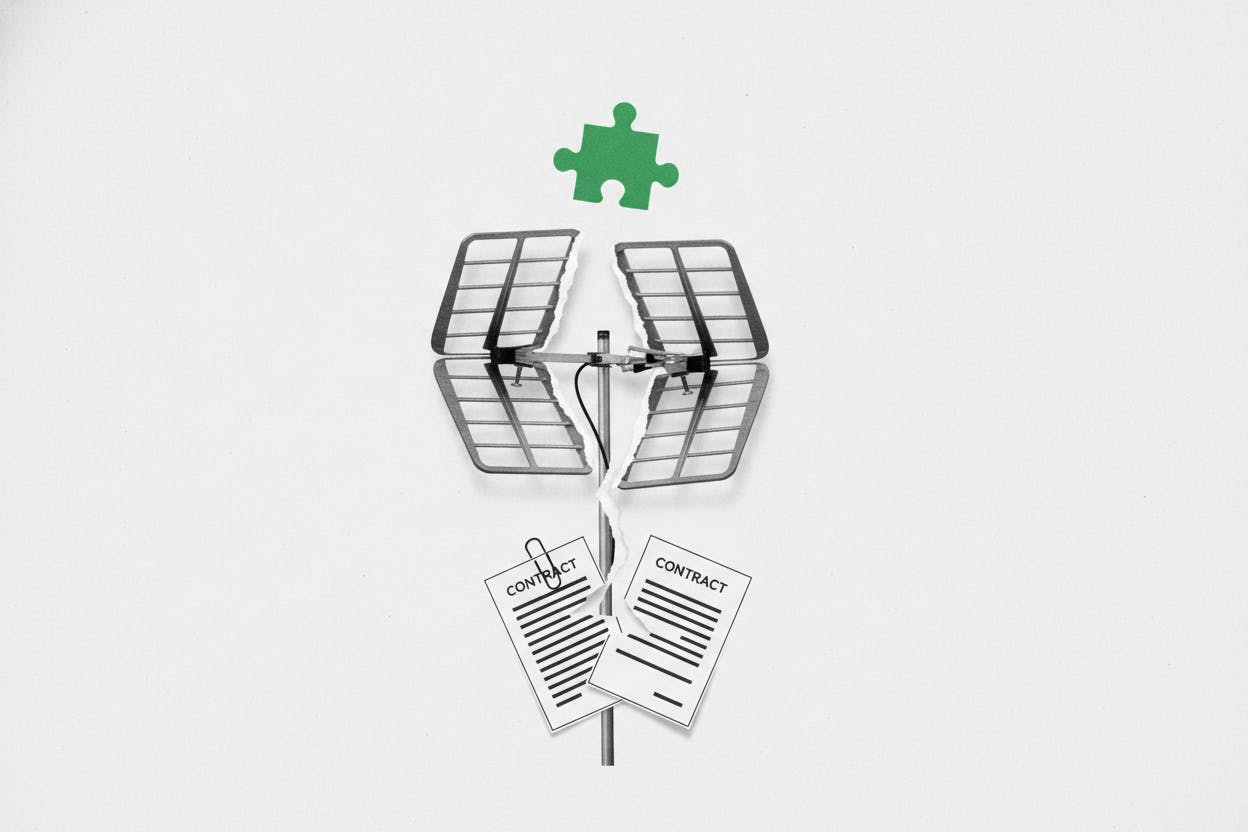

The sharp decline reflects growing investor unease about Getty's ability to close its combination with Shutterstock—a deal that was announced in early 2025 and would create a dominant player in the stock photography and editorial imagery market. Regulators in multiple jurisdictions have raised concerns about the merger's potential to reduce competition, and the companies are now working through a series of proposed remedies, including possible asset sales or licensing commitments, to win approval.

At the same time, Getty's balance sheet has come under the microscope. Leverage near 10 times EBITDA is unusually high for a company in the media and licensing space. That ratio means Getty's total debt is roughly ten times its operating profit, leaving it with limited financial flexibility. High leverage can make it harder to invest in growth, pay down debt, or weather a downturn, and it often forces companies to prioritize debt service over other spending.

Getty's business model and the merger rationale

Getty Images is a global provider of licensed visual content, including stock photos, editorial images, video footage, and related data services. Its customers range from news outlets and advertising agencies to corporate marketing departments and tech platforms. Revenue comes primarily from subscription contracts and large licensing deals, with additional income from one-off image sales and custom licensing arrangements.

The proposed merger with Shutterstock is intended to combine two of the largest players in the industry, creating scale that could lower costs, expand content libraries, and strengthen bargaining power with contributors and customers. However, the deal has drawn antitrust scrutiny because it would reduce the number of major independent stock image providers, potentially leading to higher prices or fewer choices for buyers.

Regulators in the United States, European Union, and other markets have requested additional information and are weighing whether to impose conditions—or block the deal outright. The companies have signaled they are willing to offer remedies, such as divesting certain assets or licensing content to competitors, but the process is dragging on longer than many investors expected.

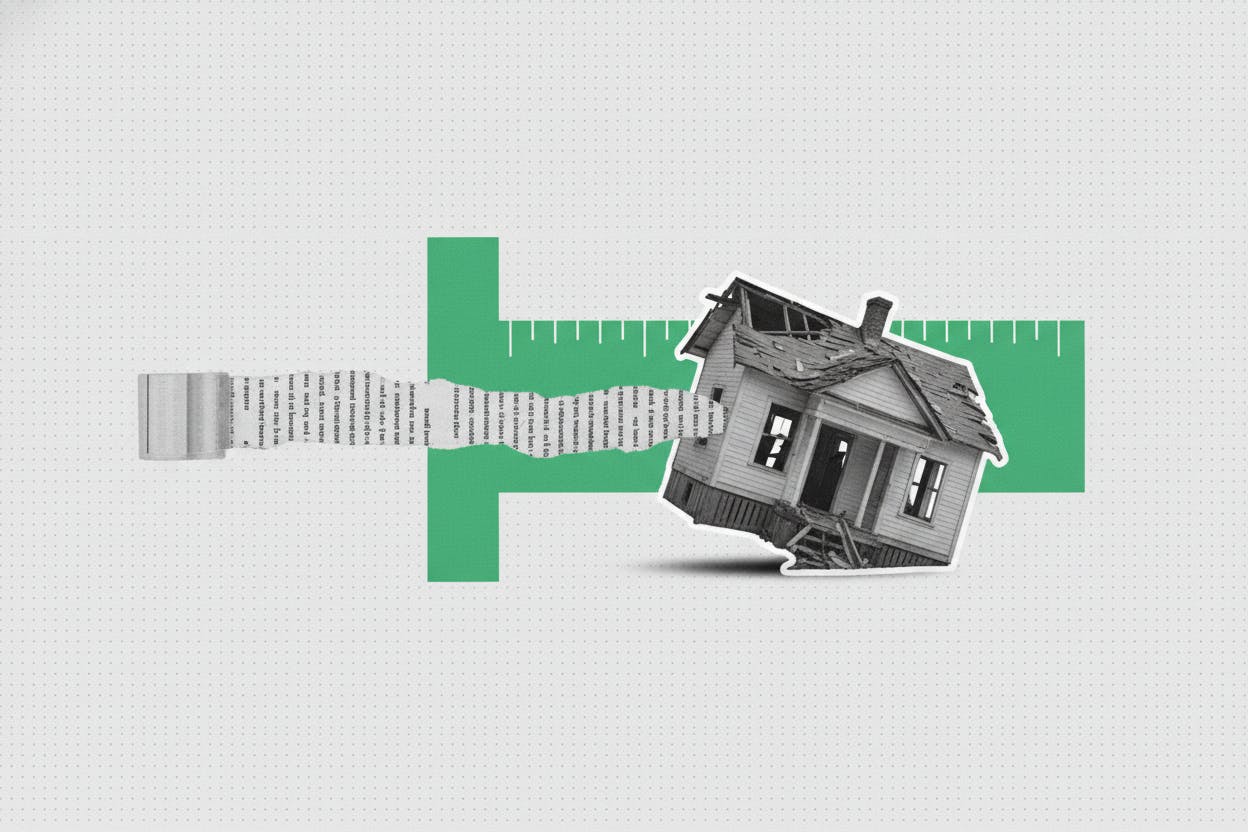

What the debt load means

Getty's leverage ratio of nearly 10 times EBITDA is a key concern for investors. For context, companies in the media and technology sectors typically carry leverage ratios between 2 and 4 times EBITDA. A ratio above 6 is generally considered aggressive, and 10 times leaves little room for error.

High leverage can amplify the impact of any revenue decline or cost increase. If Getty's earnings dip—due to a slowdown in advertising spending, for example, or a loss of customers during the merger uncertainty—the company could struggle to meet its debt obligations. That risk is reflected in the stock's steep decline, as investors price in a higher chance of financial distress.

Getty's management has said it is focused on reducing debt through cash flow generation and potential asset sales, but the merger process has complicated those efforts. Until the deal is resolved—either closed or abandoned—the company's balance sheet is likely to remain a central concern for shareholders.

What investors are watching next

For Getty Images investors, the near-term outlook hinges on two things: the fate of the Shutterstock merger and the company's ability to manage its debt load. If the deal goes through with acceptable remedies, Getty could emerge with a stronger competitive position and a clearer path to deleveraging. If it falls apart, the company may need to find another way to reduce debt, possibly through asset sales or a refinancing that could dilute existing shareholders.

The broader market backdrop also matters. A slowdown in advertising spending or a shift in how companies buy visual content could pressure Getty's revenue. Meanwhile, rising interest rates make high debt levels more expensive to service, adding another layer of risk.

For everyday investors, Getty Images illustrates the risks that can arise when a company pursues a transformative deal while carrying a heavy debt load. The stock's 44% decline over the past year is a reminder that regulatory uncertainty and financial leverage can combine to create significant downside, even for a well-known brand in a growing industry.