Investment bank Morgan Stanley has raised eyebrows in the mining sector by suggesting that Sunshine Silver Mining & Refining could significantly scale up its planned processing plant in Idaho. The bank's analysis points to recent drilling results that indicate more silver may be present in less-explored areas of the company's complex, potentially supporting a larger operation.

What Morgan Stanley is saying

Morgan Stanley's call is based on Sunshine Silver's existing resource base, which includes about 104 million ounces of silver classified as "measured and indicated" — the category with the highest geological confidence. The company also holds roughly 160 million ounces in the "inferred" category, which is less certain and requires more drilling to confirm.

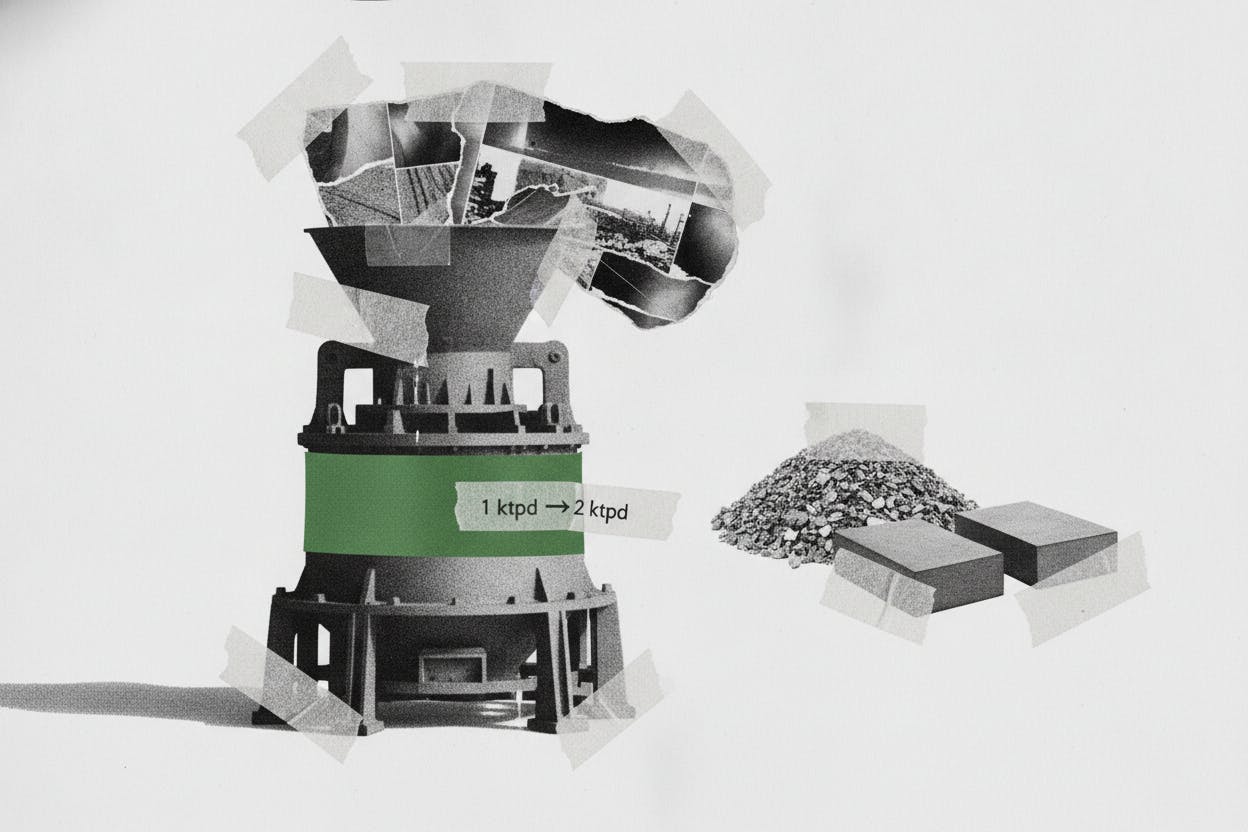

In the company's preliminary economic assessment, a 1,000-tonnes-per-day concentrator — the plant that crushes and processes ore into a sellable concentrate — supports a long operating life. Morgan Stanley argues that doubling that to a 2,000-tonnes-per-day setup could still leave 12 to 18 years of mine life, but would bring more production into the early years of the project.

That timing matters because developers and lenders value mines using discounted cash flow analysis. In plain English, dollars earned sooner count for more than dollars earned later, so front-loading production can boost a project's net present value.

The catch: reserve conversion

But a bigger plant only works on paper if drilling upgrades those resources into reserves — ore that has been proven economic and mineable. If that conversion disappoints, the upsized plan may not be financeable, and the market will likely treat the project's timeline as less certain.

This is a common challenge for mining developers. Many companies boast large resource figures, but only a fraction become reserves that can support a bankable feasibility study and secure project financing. Investors have seen this play out before with other miners, such as First Majestic Silver, which committed $12 million to expand its Santa Elena mine after clearing permitting hurdles.

Morgan Stanley's $23 price target for Sunshine Silver is really a bet on reserve conversion, not just the 2,000-tonnes-per-day headline. The bank is essentially saying that if Sunshine can drill, model, and permit its way from a big resource estimate to bankable reserves, the higher throughput could unlock significant value.

What it means for investors

For everyday investors, the key takeaway is that valuation metrics like net present value per share are more sensitive to execution risk than to the company's top-line ounces-in-the-ground figure. A larger resource base is nice, but it's the conversion to reserves that drives financing and ultimately production.

Investors should watch for upcoming drilling results and feasibility study updates from Sunshine Silver. The company will need to demonstrate that it can upgrade its inferred resources to measured and indicated categories, and then prove that those resources can be mined economically at the higher throughput rate.

The broader market context also matters. Silver prices have been volatile, and mining costs have risen across the industry. A larger concentrator means higher upfront capital costs, which could strain a developer's balance sheet if metal prices fall. That's why Morgan Stanley's analysis focuses on the discounted cash flow math — it accounts for both the timing of production and the risk of future price changes.

Other mining companies have faced similar challenges. Sinda's NYSE debut fell 10% as mining IPOs face investor skepticism, highlighting the market's wariness of development-stage miners. And EACON's autonomous mining truck IPO in Hong Kong shows that investors are looking for efficiency gains in mining operations.

The bottom line

Morgan Stanley's view on Sunshine Silver is a vote of confidence in the company's resource base, but it comes with a clear caveat: the bigger plant only adds value if the drilling delivers. Until that happens, investors should treat the project's timeline and valuation as uncertain, and focus on the company's ability to execute on its exploration and permitting plans.

For those following the silver mining space, Sunshine Silver's progress will be a test case of whether a mid-tier developer can bridge the gap between a large resource and a bankable mine plan. The answer will determine whether Morgan Stanley's $23 target is a realistic goal or just a paper exercise.