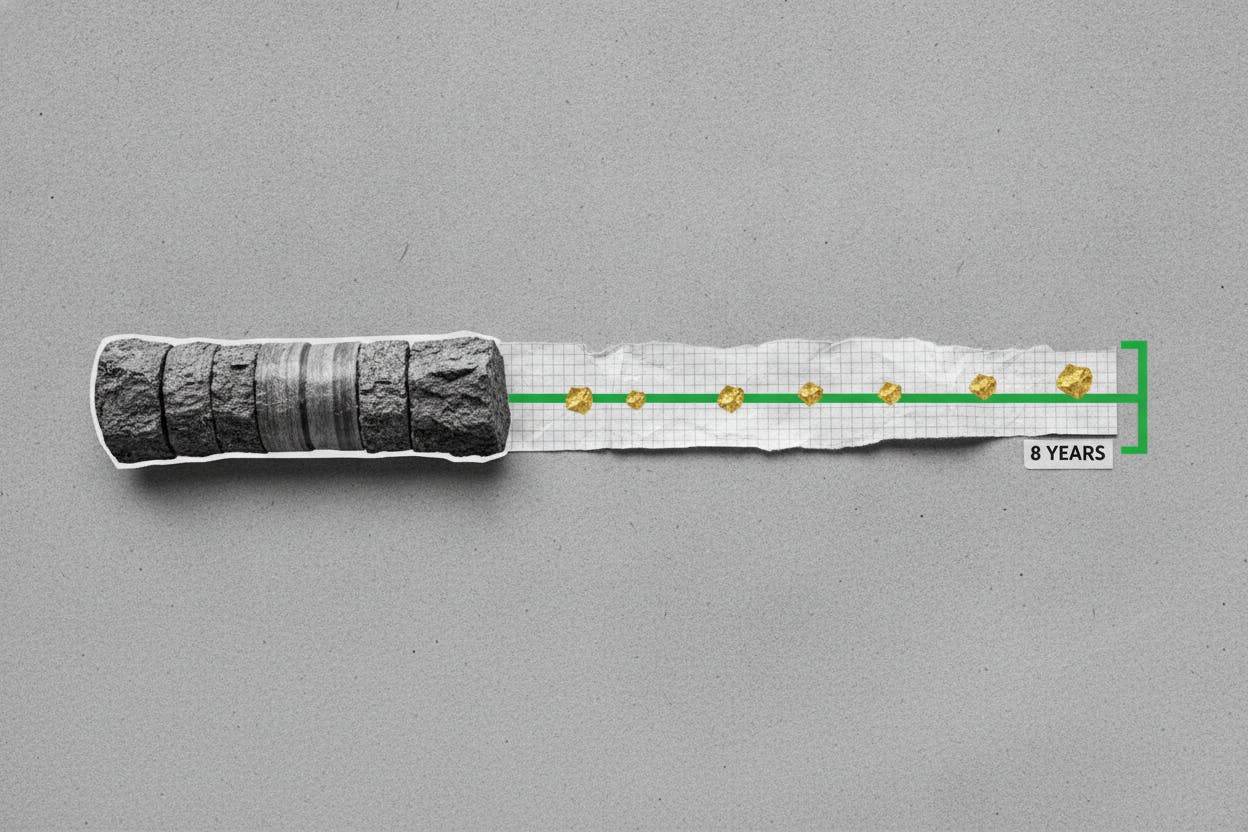

Wesdome Gold Mines, a Canada-listed gold producer, has given investors a clearer picture of its future. In a reserve and resource update effective December 31, 2025, the company reported that its proven and probable reserves now stand at about 1.4 million ounces of gold. That is enough to keep its Eagle River and Kiena mines running for roughly eight years at current production rates.

The news comes as Wesdome also raised its 2028 production target to between 185,000 and 230,000 ounces, up from a previous range of 180,000 to 205,000 ounces. The company expects Eagle River to produce 100,000 to 120,000 ounces in 2027 and 2028, while Kiena should reach 85,000 to 110,000 ounces by 2028.

What drove the reserve increase?

The biggest jump came at Eagle River, where proven and probable reserves rose by 39%. That is a meaningful gain for a mine that has been in operation for decades. The company also reported a sharp increase in what miners call “inferred resources” — early-stage estimates that are not yet reliable enough to be classified as reserves but could become mineable after more drilling. Inferred resources jumped 87% to roughly 1.2 million ounces.

For context, a reserve is gold that a company has drilled in enough detail to know it can be mined profitably. An inferred resource is a less certain estimate, often based on wider-spaced drilling. While it cannot be counted in a mine plan today, it represents potential future ore. Wesdome’s large inferred resource pool gives it a pipeline to replace reserves as they are mined.

Costs remain in focus

Just as important as the production numbers is what Wesdome expects to spend getting that gold out of the ground. The company said its all-in sustaining costs (AISC) — a key industry metric that includes operating costs plus the money needed to keep a mine running — should stay mostly in line with its 2026 guidance of $1,525 to $1,700 per ounce.

That is notable because rising costs have been a persistent headache for gold miners in recent years. Labour, energy, and equipment expenses have all climbed, squeezing margins even when gold prices are high. By keeping its cost outlook stable, Wesdome is signalling that it believes it can grow production without letting expenses spiral.

The company also confirmed it will continue paying a quarterly dividend of C$0.0306 per share and has expanded its share buyback plan to 9.0 million shares under a normal course issuer bid. That represents about 6% of its public float.

What it means for investors

For gold mining investors, a larger proven-and-probable reserve base is more than just a bigger number. It reduces the risk that a mine runs out of ore sooner than expected, which makes cash-flow forecasts less speculative. That is especially important for companies like Wesdome that return cash to shareholders through dividends and buybacks.

By pairing reserve growth with a cost outlook that stays near its 2026 range, Wesdome is trying to address two common concerns in the mining sector: depletion risk and cost overruns. Investors will now watch whether the planned production ramps at Eagle River and Kiena can actually deliver those 2027 and 2028 ounce targets at the stated cost levels. That is what ultimately supports ongoing shareholder returns.

The broader backdrop for gold miners remains mixed. Gold prices have been volatile, and while they remain elevated by historical standards, input costs have also risen. Companies that can grow reserves and production without blowing up their cost structures tend to be rewarded by the market.

Wesdome’s update gives investors a clearer line of sight on the next several years. The eight-year mine life provides a solid foundation, and the increased inferred resources offer a potential buffer for the future. Whether the company can execute on its plans will determine if the stock becomes a favourite among gold-focused investors.