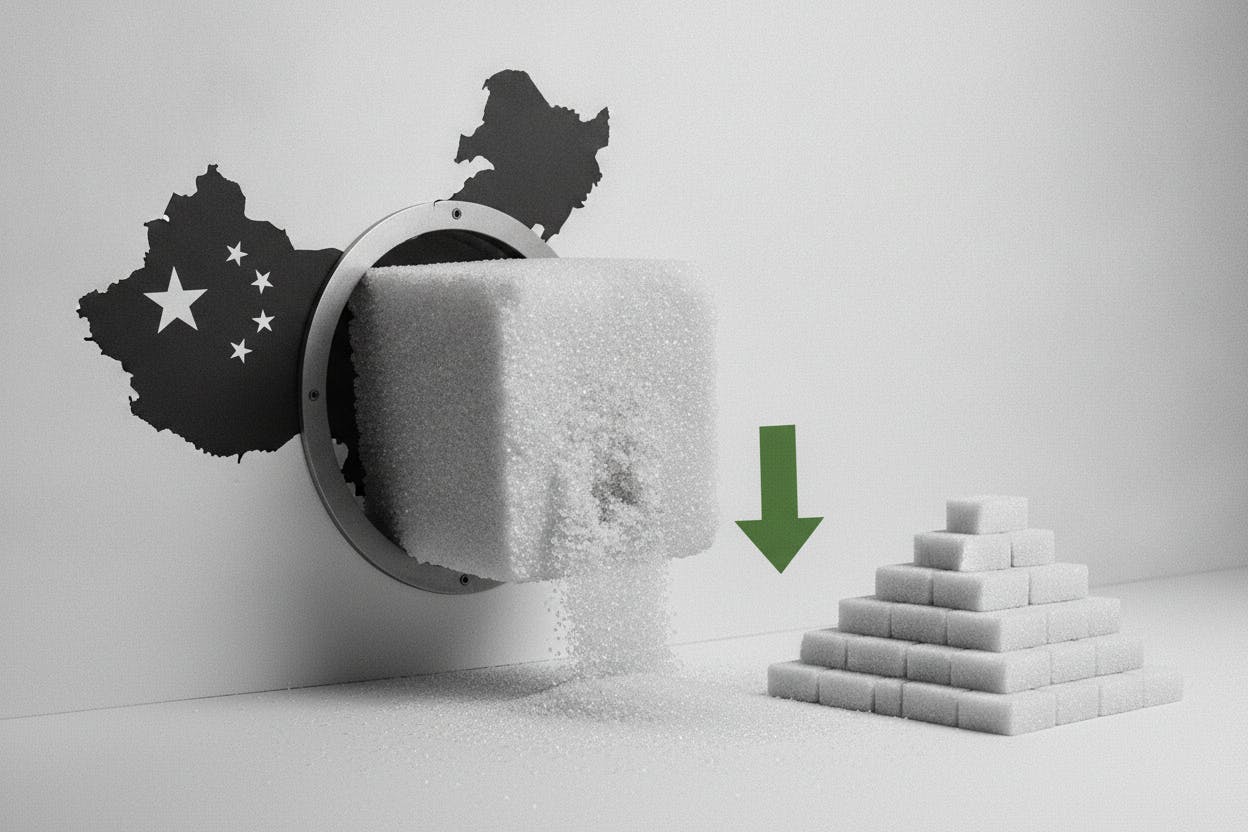

The expiration of ICE's July raw sugar futures contract this week saw an unusually large handoff into physical supply, with traders estimating 15,678 lots delivered—equivalent to about 796,500 metric tons. Preliminary figures from two traders indicated that China's state-owned COFCO was the only seller making delivery, a rare concentration that caught market attention.

On the buying side, Sucden emerged as the biggest receiver, followed by Louis Dreyfus, Bunge, and Wilmar. The volume underscores the scale of physical sugar trading tied to futures markets, where contracts nearing expiration often result in actual commodity delivery rather than cash settlement.

What Happens When a Futures Contract Expires

Futures contracts are standardized agreements to buy or sell a commodity at a predetermined price on a set date. Most traders close out positions before expiration to avoid taking or making physical delivery. But when a contract expires, holders who haven't offset their positions must either deliver the commodity (if they sold) or accept it (if they bought).

The July raw sugar contract's expiration is a routine event, but the size of deliveries—nearly 800,000 tonnes—is notable. For context, ICE raw sugar futures trade in lots of 112,000 pounds (about 50.8 metric tons). A single seller dominating deliveries is less common and can signal strategic positioning by a major producer or trader.

COFCO, China's largest food and agricultural conglomerate, has a significant global sugar footprint, including refineries and trading operations. Its role as the sole deliverer suggests it had accumulated a large short position—betting on falling prices—and chose to fulfill it with physical sugar rather than buying back contracts.

What It Means for Sugar Markets and Investors

For everyday investors, this news offers a window into how physical commodity markets operate behind the scenes. Sugar prices are influenced by global supply-demand dynamics, weather in key growing regions like Brazil and India, and policy moves by major producers. The large delivery may reflect COFCO's view on near-term supply or its need to move inventory.

Investors in sugar-related stocks or ETFs—such as those tracking agricultural commodities—should note that large deliveries can sometimes signal ample supply, which may weigh on prices. However, the expiration itself is a technical event, not a fundamental shift. The real drivers remain global production forecasts, ethanol demand (which competes with sugar for cane), and trade policies.

For those holding positions in sugar futures or options, the expiration highlights the importance of monitoring contract roll dates. Traders who don't intend to take delivery must close or roll positions before expiry to avoid unexpected obligations.

Broader Context: Commodity Markets and Physical Delivery

Physical delivery in futures markets is a key mechanism that keeps futures prices aligned with spot prices. Without it, futures could diverge from reality. The July contract's delivery pattern—one dominant seller and multiple large receivers—is typical of markets where a few major players control significant storage and logistics.

Similar dynamics play out in other commodities. For example, US natural gas futures recently saw their July contract expire with a different pattern, reflecting the unique storage and pipeline constraints of that market. In both cases, the expiration process provides transparency into who holds physical supplies.

The involvement of global traders like Sucden, Louis Dreyfus, Bunge, and Wilmar—all major agricultural commodity houses—underscores the interconnected nature of food supply chains. These firms often use futures to hedge their physical positions, and deliveries can be part of normal inventory management.

What Investors Should Watch Next

While the July expiration is now history, attention shifts to the August and October contracts. Sugar prices have been volatile in recent months due to weather concerns in Brazil and India's export policies. The large delivery may temporarily ease supply concerns, but the market will quickly refocus on new-crop forecasts.

For investors in agricultural commodities, the key takeaway is that futures expiration data can offer clues about physical market tightness. A single seller delivering a huge volume might indicate that a major player is reducing inventory, or that it expects lower prices ahead. Conversely, strong demand from receivers could signal that end-users are securing supply.

As always, commodity investing carries risks from weather, geopolitics, and currency moves. The sugar market is no exception. But understanding the mechanics of futures delivery helps investors interpret price moves and avoid surprises during contract roll periods.