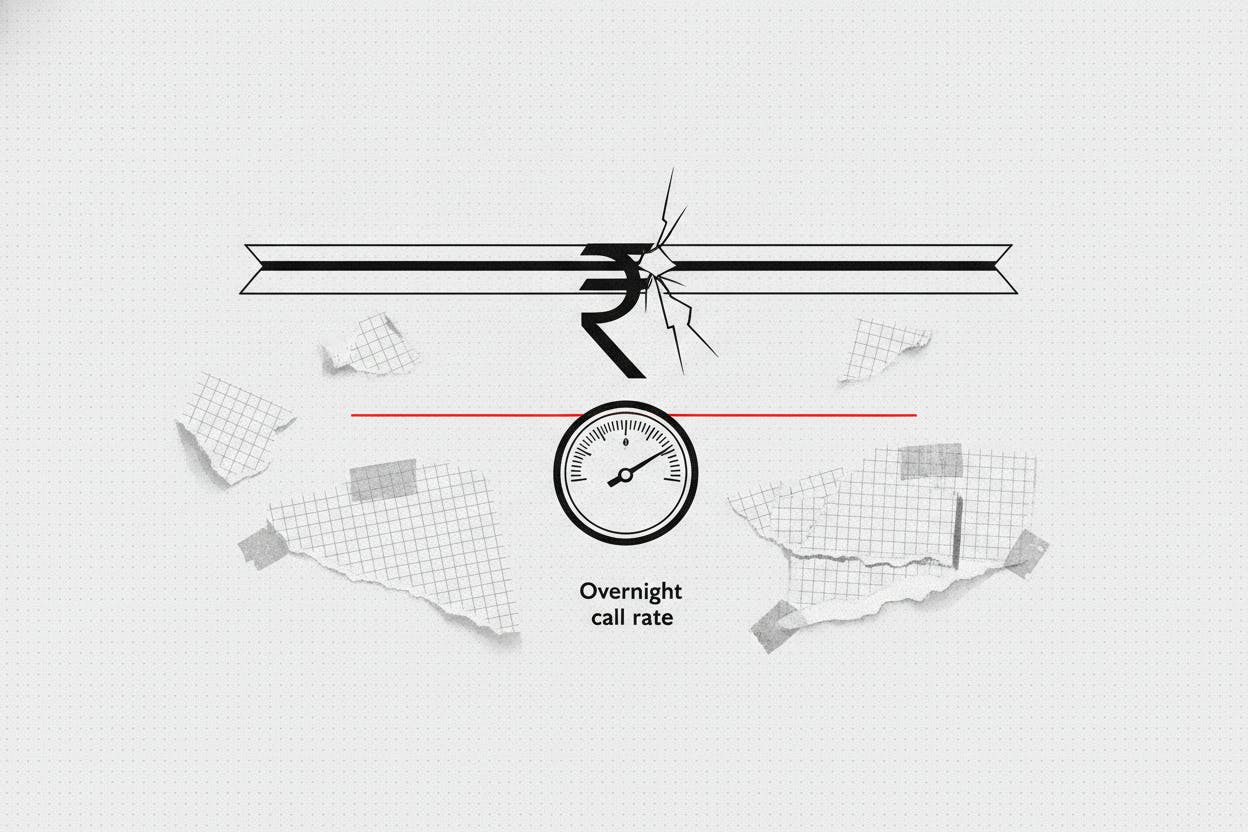

India's overnight interbank borrowing cost briefly broke through the Reserve Bank of India's (RBI) usual ceiling on Tuesday, signaling that a prolonged cash shortage is straining the country's money markets. According to Reuters, the call money rate—the rate at which banks lend to each other overnight—hit 5.65%, above the central bank's 5.50% marginal standing facility (MSF) rate.

The move came after eight consecutive days of systemwide liquidity deficit through June 29, with the weighted average call rate (WACR) also climbing to 5.50%, the top of the RBI's interest-rate corridor. This suggests that the average cost of overnight funding is now sitting at the upper bound of the central bank's comfort zone, rather than near its policy rate.

What Is the Interest-Rate Corridor and Why Does It Matter?

The RBI manages short-term interest rates through a system known as the interest-rate corridor. At the center is the repo rate, currently 5.25%, which is the rate at which the RBI lends to banks. The MSF rate, set at 5.50%, acts as a ceiling: banks can borrow from the RBI at this rate when they need emergency funds. In theory, this should cap how high the market overnight rate can go, because banks would rather borrow from the central bank than pay more in the interbank market.

When the call money rate rises above the MSF, it indicates that something is amiss in the money-market plumbing. It suggests that some banks are unable to access the MSF—perhaps due to collateral constraints or limits on who can borrow from whom—and are forced to pay a premium in the interbank market. This is a sign of friction, not just a simple shortage of cash.

Reuters noted that recent RBI cash injections via repo operations were under-subscribed, meaning banks did not take up all the liquidity the central bank offered. This could reflect banks' reluctance to borrow at the repo rate due to their own balance-sheet constraints or a preference to hold onto cash for regulatory reasons.

What This Means for Investors

For everyday investors, the immediate impact is on short-term borrowing costs. When the overnight rate trades above the MSF, it can reset market expectations for where risk-free short-term money is priced, even without a change in the RBI's repo rate. If this persists, the WACR tends to stay elevated, and that can spill into the pricing of other very short-dated instruments, such as Treasury bills and banks' short-term funding like certificates of deposit and commercial paper.

In other words, funding conditions can tighten at the front end of the curve before policymakers do anything on the headline policy rate. This could mean higher borrowing costs for companies that rely on short-term debt, and potentially lower returns for investors in money-market funds or short-term bonds.

The broader context is that India's banking system has been grappling with a liquidity squeeze for weeks. The RBI has been injecting cash through open-market operations, but the under-subscription of recent repo auctions suggests that the problem is not just about the amount of cash, but about how it flows through the system. This is reminiscent of similar episodes in other emerging markets, where tight liquidity has led to spikes in overnight rates even when central banks were trying to ease.

Investors should watch for any signs that the RBI might adjust its liquidity management tools, such as increasing the frequency or size of repo operations, or even cutting the cash reserve ratio (CRR) to free up more funds for banks. If the tightness persists, it could also influence the RBI's stance on interest rates, though the central bank is currently focused on supporting growth.

For now, the spike in the call money rate is a reminder that even in a well-managed system, frictions can emerge. It is not a crisis, but it is a signal that the cost of short-term money is rising, and that could have ripple effects across the financial system.