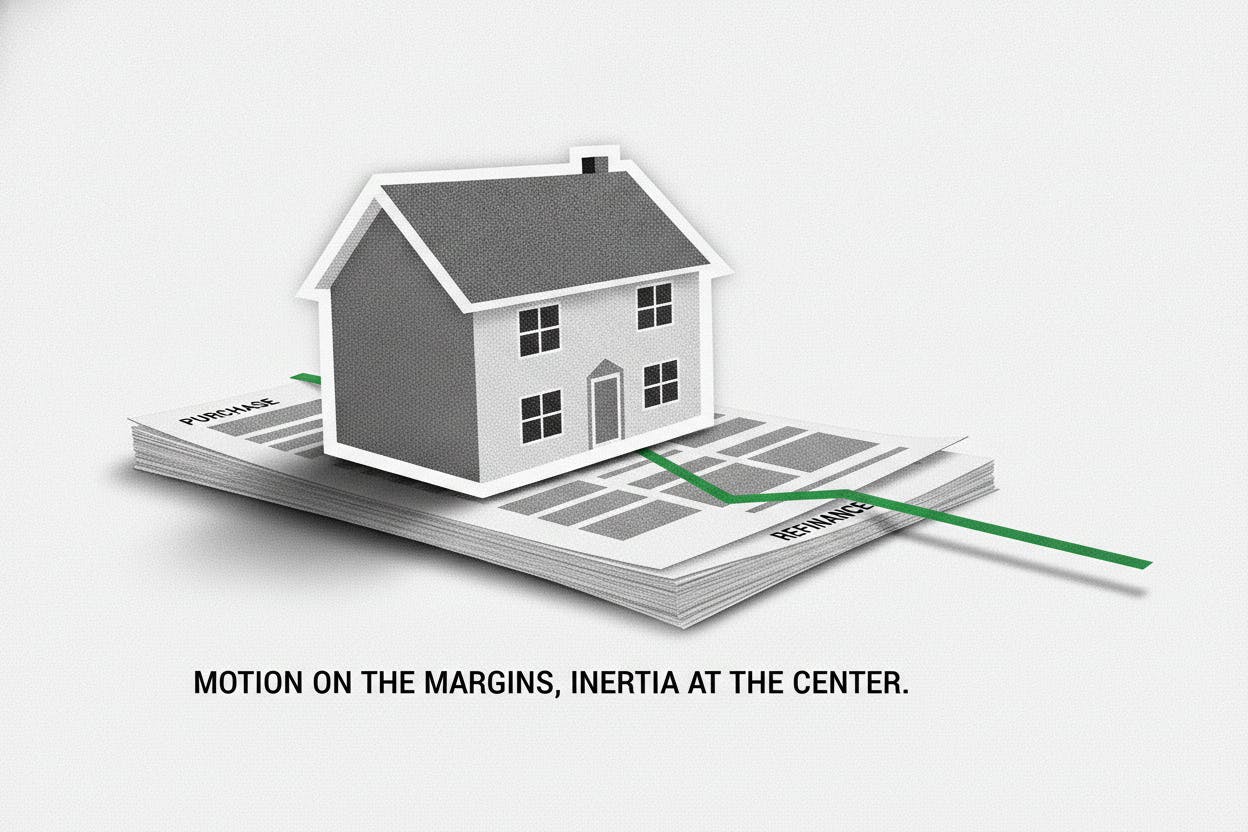

The US mortgage market showed signs of strain last week as the average 30-year fixed rate climbed to 6.65%, its highest level since August 2025, prompting a drop in overall mortgage applications. Data from the Mortgage Bankers Association (MBA), an industry trade group, revealed total applications fell 2.7% for the week ended July 10, following a holiday-distorted dip the prior week.

The decline was not uniform across all loan types. Purchase applications, which track homebuyer demand, slid a seasonally adjusted 7% compared to the previous week. Meanwhile, refinancing activity rose 4%, even as the average 30-year rate edged up from 6.58% to 6.65% for loans of $832,750 or less.

Why Purchase Demand Is Falling

Higher borrowing costs directly hit homebuyers' wallets. At 6.65%, the monthly payment on a typical mortgage is noticeably higher than it was just a few months ago, and more households are failing lenders' debt-to-income checks. MBA economist Joel Kan noted that purchase applications have slipped below last year's pace, underscoring how quickly rising rates can cool buyer enthusiasm.

This trend mirrors broader economic pressures. The Federal Reserve's campaign to tame inflation has kept short-term interest rates elevated, and long-term bond yields—which influence mortgage rates—have followed suit. For everyday investors, the message is clear: when mortgage rates rise, housing affordability tightens, and fewer buyers can qualify for loans. That can slow home price growth and reduce transaction volumes, which may weigh on homebuilder stocks and related sectors.

Refinancing Bucks the Trend

While purchase demand slumped, refinancing activity actually increased. The 4% rise in refinance applications was driven by borrowers using government-backed loan programs. Federal Housing Administration (FHA) refinances jumped 9%, and Department of Veterans Affairs (VA) refinances climbed 10%. These borrowers often have access to streamlined refinancing options with less paperwork, or they are replacing loans taken out at even higher rates in the past.

This split highlights a key nuance: the mortgage market is not a monolith. Even as rates rise, some homeowners can still lower their monthly payments by refinancing, especially if they originally locked in a rate above 7% or 8%. However, the overall pool of eligible refinancers is shrinking, as most homeowners already have rates below 6% from the pandemic era.

What It Means for Investors

For everyday investors, the latest MBA data offers a window into the health of the housing market and the broader economy. When purchase applications fall, it suggests that higher rates are dampening demand, which could eventually lead to slower home price appreciation or even price declines in some markets. That might be a headwind for real estate investment trusts (REITs), homebuilders, and lenders.

On the other hand, the uptick in refinancing—especially among FHA and VA borrowers—shows that some segments of the market are still finding ways to manage costs. This resilience could support consumer spending, as lower monthly payments free up cash for other expenses.

Investors should also watch how the Federal Reserve responds. If mortgage rates stay elevated, it could further cool the housing market, which is a key driver of economic growth. However, if inflation continues to ease, the Fed may eventually cut rates, which would likely lower mortgage rates and reignite demand.

For context, the broader economic backdrop remains mixed. Recent data on US small business optimism showed a slight uptick in June, but high rates continue to restrain hiring and spending. Similarly, the banking sector is navigating higher rates, as seen in M&T Bank's Q2 profit rise, where higher lending spreads boosted earnings. Yet, rising funding costs are a concern for some lenders, as highlighted by Danske Bank's recent report.

The Bottom Line

Mortgage rates at 6.65% are creating a two-speed market: homebuyers are pulling back, while a narrower group of government-backed borrowers is still refinancing. For investors, this means housing-related stocks and bonds could face headwinds in the near term, but the refinancing uptick offers a silver lining. As always, the path of rates will depend on inflation data and Fed policy, so keeping an eye on economic releases is key.