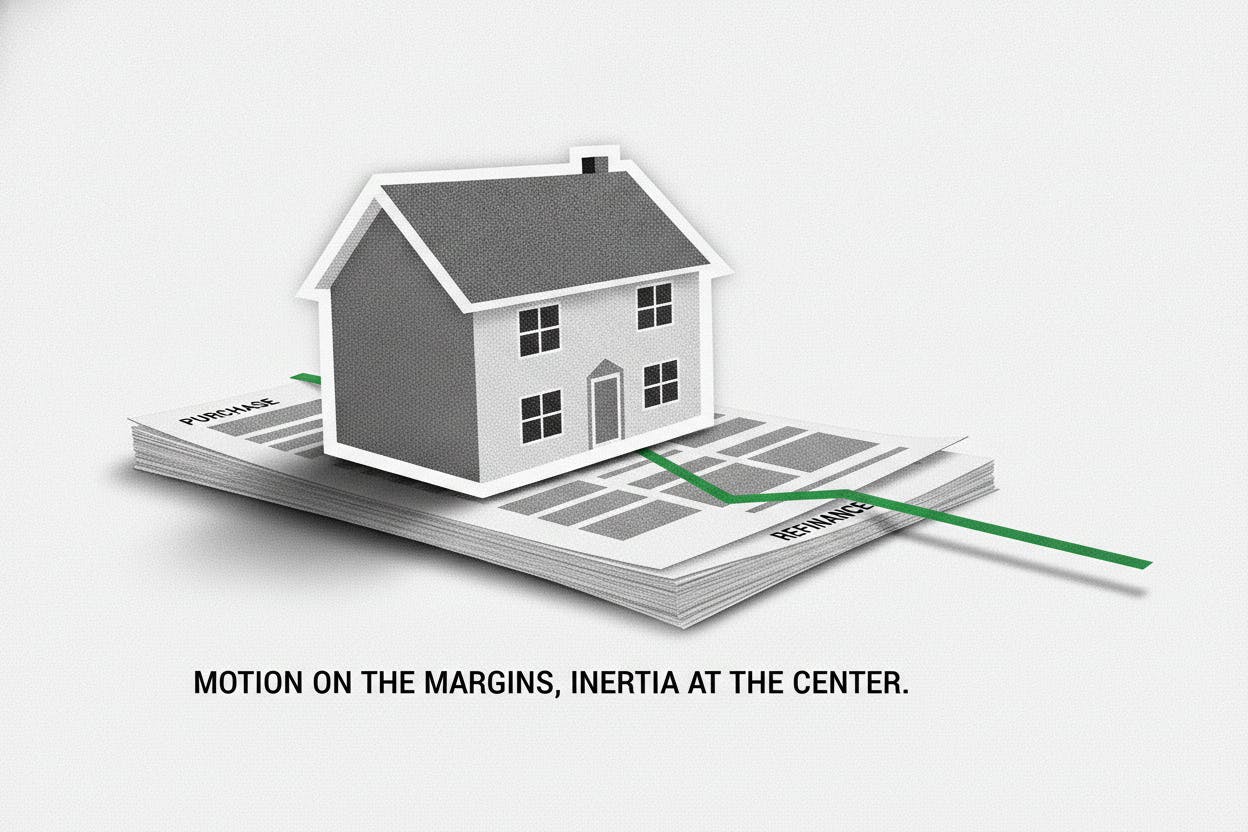

The Mortgage Bankers Association (MBA) reported a 1% seasonally adjusted increase in mortgage applications for the week ended June 19, but the headline number masks a split market. Refinancing activity rose 3% week over week, while purchase applications fell 1%, highlighting how different borrowers are responding to the same interest rate environment.

What the Data Shows

The MBA's market composite index, a broad measure of mortgage application volume, rose 1% on a seasonally adjusted basis. However, the unadjusted index fell 10% from the prior week, reflecting adjustments for the Juneteenth holiday. The refinance index climbed 3%, while the seasonally adjusted purchase index slipped 1%.

Interest rates barely budged. The average 30-year fixed conforming rate eased slightly to 6.59% from 6.6%, and the 15-year rate held steady at 6.02%. This stability came even after the Federal Open Market Committee struck a more hawkish tone at its June meeting, signaling that rate cuts may not come as quickly as some had hoped.

MBA chief economist Mike Fratantoni noted that overall application volume is running 8% above year-ago levels. The share of FHA loans ticked up to 17.9% from 17.5%, suggesting that affordability-focused borrowers remain active in the market.

Why Refinancers and Buyers Are Reacting Differently

The divergence between refinancing and purchase demand is a reminder that small rate moves affect borrowers differently. Refinancing is essentially a break-even calculation: if a slightly lower rate reduces monthly payments enough to recoup closing costs within a reasonable timeframe, homeowners can act quickly. A modest dip in rates can therefore bring a wave of refinancing inquiries.

Buying a home is a bigger financial commitment. Even if the rate falls a few basis points, would-be buyers still face the full purchase price and must qualify for a large new monthly payment. That makes purchase demand less sensitive to small rate changes, which helps explain why it can remain soft even when refinancing shows signs of life.

For context, the housing market has been grappling with elevated mortgage rates for over a year. The 30-year rate has hovered in the 6.5% to 7% range for much of 2024, well above the sub-3% levels seen in 2020 and 2021. That has priced out many first-time buyers and kept existing homeowners locked into lower-rate mortgages, reducing inventory and sales volumes.

What It Means for Investors

For everyday investors, this data offers a window into consumer behavior and the housing market's pulse. A rise in refinancing suggests that some homeowners are still able to benefit from rate dips, which could support consumer spending by freeing up cash flow. But the persistent weakness in purchase demand signals that affordability remains a major hurdle, particularly for younger buyers.

The uptick in FHA loan share is another clue: these government-backed loans are popular with first-time buyers and those with smaller down payments. A rising share suggests that more buyers are stretching to enter the market, which could be a sign of both demand and financial strain.

Investors should also watch how the Federal Reserve's next moves affect mortgage rates. The Fed has held its benchmark rate steady since July 2023, but recent inflation data has been stickier than expected, delaying hopes for rate cuts. If the Fed eventually lowers rates, mortgage rates could follow, potentially boosting both refinancing and purchase activity. But if rates stay elevated, the current pattern—modest refinancing upticks alongside soft purchase demand—could persist.

Broader economic indicators, such as employment and wage growth, will also play a role. A strong labor market supports housing demand, but high rates and home prices continue to squeeze affordability. The MBA's weekly data will remain a key gauge for tracking how these forces play out.

For now, the message is clear: small rate moves matter more to refinancers than to homebuyers, and the housing market remains in a waiting game for more significant shifts in borrowing costs.