Wise, the cross-border payments company, has announced its largest-ever share buyback program—worth more than $500 million—alongside its fiscal 2026 results. The announcement marks the company's first earnings report since shifting its primary listing to the United States, a move that signals its growing focus on American investors.

How the Buyback Is Structured

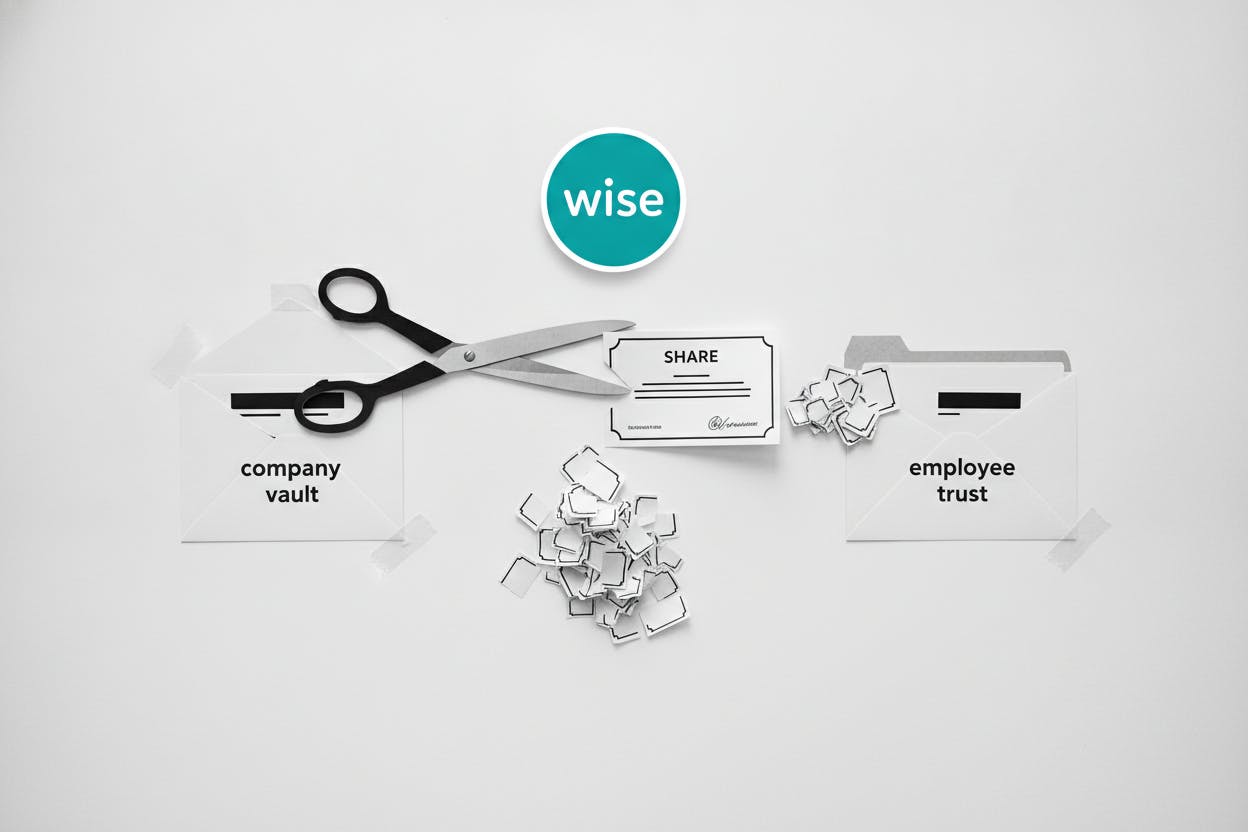

The company plans to split the repurchases into two distinct buckets. About 60% of the buyback will go toward shares bought into treasury—stock that the company holds on its balance sheet. The remaining 40% will fund Wise's recurring employee share trust, which supplies stock for staff equity awards.

This split matters because buybacks only boost per-share metrics if they reduce, or at least stop growth in, the diluted share count. The diluted share count includes not just outstanding shares but also potential shares from employee stock options and other equity awards. By routing a portion of the buyback through the employee share trust, Wise can meet its equity compensation obligations without issuing as many new shares—an anti-dilution measure that helps preserve the buyback's benefits.

Financial Performance

For the year ended March 31, Wise reported net revenue of $2.50 billion, up 19% year-over-year. However, net income fell to $498.7 million from $550.3 million in the prior year. The company framed the buyback plan as a flexible use of cash that it intends to revisit annually, while keeping its medium-term growth outlook broadly intact.

The revenue growth reflects continued expansion in Wise's core cross-border payments business, which allows individuals and businesses to send money internationally at lower costs than traditional banks. The decline in net income, meanwhile, may reflect higher operating expenses or investment costs as the company scales.

What It Means for Investors

For everyday investors, the headline $500 million figure is less important than where the stock ends up. The 60-40 split between treasury shares and the employee trust creates a test of share-count control. The portion held in treasury can more directly tighten supply over time—especially if shares are kept off-market or eventually canceled. The employee trust portion, by contrast, is essentially a tool to manage dilution from staff equity awards.

Investors will focus on whether the program actually pulls the diluted share count down, or mainly keeps it from creeping higher. That distinction drives long-run earnings per share, a key metric for valuing any stock. If Wise can reduce its diluted share count over time, each remaining share represents a larger slice of the company's profits.

Wise's move comes amid a broader trend of companies using buybacks to return capital to shareholders. For context, other firms have also turned to share repurchases and convertible notes to manage their capital structures. For example, Nuvation Bio upsized its convertible note deal to $250 million, setting a conversion price that reflects similar capital management strategies.

Broader Market Context

The buyback announcement also comes as currency markets face pressure from a strong US dollar. The yuan headed for its biggest weekly drop since March as the dollar strengthened, a dynamic that could affect Wise's cross-border payment volumes. A stronger dollar makes it more expensive for non-US customers to send money to dollar-denominated destinations, potentially impacting transaction growth.

Wise's shift to a US primary listing also aligns with a broader trend of companies moving their stock listings to the US to access deeper capital markets. Similar moves have been seen in other sectors, such as NetEase upgrading its Hong Kong listing status as trading shifts east.

Looking Ahead

Management has indicated that the buyback program is flexible and will be reviewed annually. This gives Wise the ability to adjust the pace of repurchases based on business conditions and cash flow. The company's medium-term growth outlook remains broadly intact, suggesting that management sees the buyback as a way to reward shareholders without sacrificing investment in growth.

For investors, the key takeaway is to watch the diluted share count in future earnings reports. If Wise can demonstrate that the buyback is actually reducing the number of shares outstanding—rather than just offsetting dilution from employee equity—it could provide a meaningful boost to earnings per share over time.