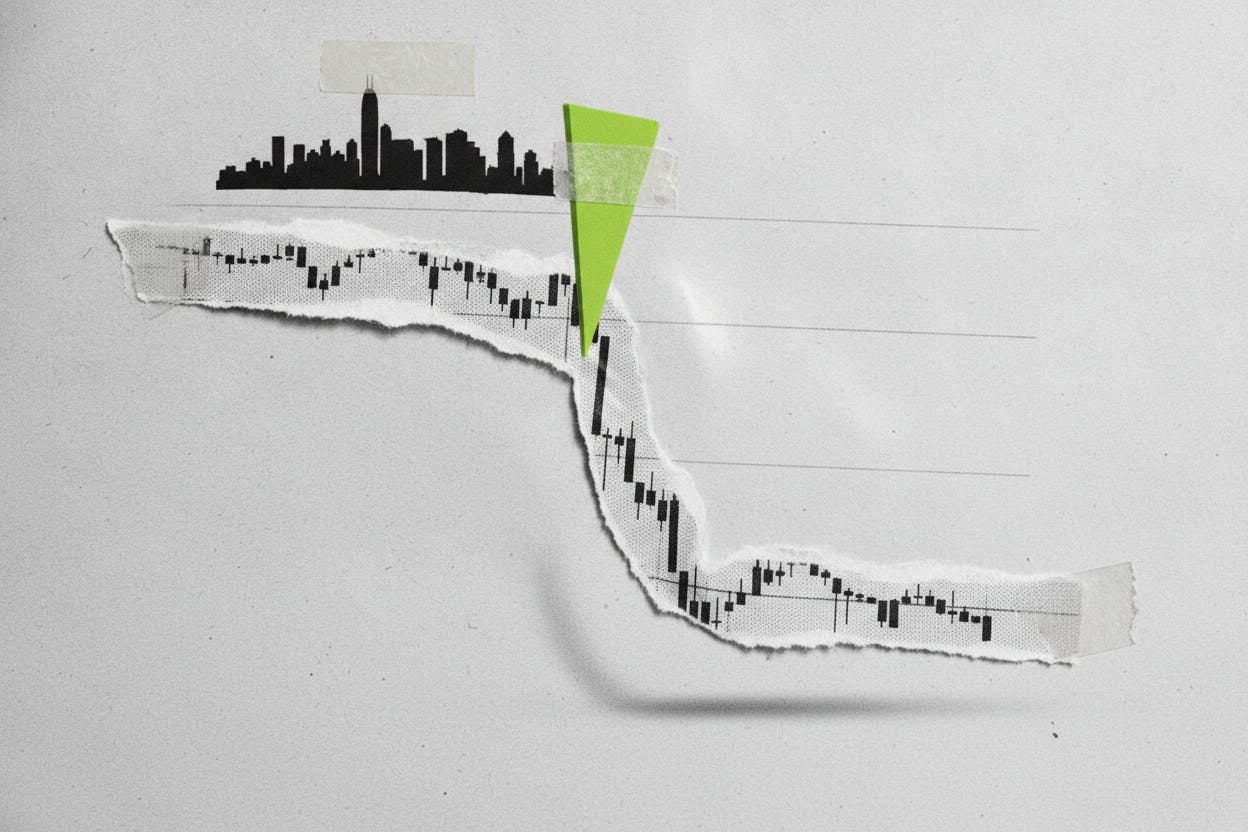

Hong Kong stocks edged lower on Tuesday, with the benchmark Hang Seng Index falling 0.6%, as investors grappled with a fresh wave of Middle East uncertainty and growing expectations that the Federal Reserve could raise interest rates again in September.

The decline came as traders kept a close eye on possible talks between the United States and Iran, which could have significant implications for energy markets and global stability. At the same time, market pricing now suggests a 64% probability that the Fed will deliver another rate hike at its September meeting, a shift that has weighed on risk appetite across Asian markets.

Middle East Tensions Return to the Fore

Geopolitical risks in the Middle East have re-emerged as a key concern for investors, with reports of potential US-Iran negotiations adding to the uncertainty. The region has been a flashpoint for volatility in recent months, particularly around the Strait of Hormuz, a critical chokepoint for global oil shipments. Any disruption there could send energy prices sharply higher, feeding into inflation concerns worldwide.

This backdrop has kept traders cautious. While talks could signal a de-escalation, the mere possibility of diplomatic engagement often creates a wait-and-see mood in markets. For Hong Kong stocks, which are heavily influenced by global trade and sentiment, such uncertainty tends to dampen buying activity.

Related coverage: Oil Slips 1% as US-Iran Talks in Doha Leave Traders Guessing on Strait of Hormuz Risk

Fed Rate Hike Bets Resurface

Adding to the pressure on Hong Kong stocks was a shift in expectations for US monetary policy. Traders are now pricing in a 64% chance that the Federal Reserve will raise its benchmark interest rate at the September meeting, according to CME Group's FedWatch tool. That marks a notable increase from just a few weeks ago, when markets were more evenly split on the likelihood of further tightening.

The Fed has been on a campaign to tame inflation, raising rates aggressively over the past year. While inflation has cooled from its peaks, it remains above the central bank's 2% target, leaving the door open for additional hikes. Higher interest rates tend to make stocks less attractive by increasing borrowing costs for companies and reducing the present value of future earnings. They also strengthen the US dollar, which can put pressure on emerging markets like Hong Kong.

This dynamic has been a recurring theme for Asian markets. For instance, Indian stocks slipped recently as IT shares dropped on US rate worries, highlighting how Fed policy ripples through global equity markets.

What It Means for Investors

For everyday investors, the combination of geopolitical tensions and rate hike expectations creates a challenging environment. The Hang Seng's 0.6% decline is modest, but it reflects a broader caution that could persist until there is more clarity on both fronts.

Geopolitical events are notoriously hard to predict, but their market impact is often short-lived unless they escalate into sustained disruptions. Investors should watch for any concrete developments from US-Iran talks, as a breakthrough could ease tensions and boost risk appetite, while a breakdown might fuel further volatility.

On the monetary policy side, the key data point to monitor is the next US inflation report, due in August. A hotter-than-expected reading could solidify the case for a September hike, while a cooler number might reduce the probability. For now, the 64% probability suggests the market is leaning toward a hike, but that figure can shift quickly with new data.

In this environment, diversification remains a prudent strategy. Sectors that tend to perform well during periods of rising rates, such as financials, may offer some buffer, while growth stocks—particularly in tech—could face headwinds. Hong Kong's market is also sensitive to China's economic outlook, which has shown signs of stabilization, as seen in China AI and chip stocks rallying on factory activity returning to growth in June.

Overall, the Hang Seng's dip is a reminder that global markets remain at the mercy of two powerful forces: geopolitics and central bank policy. Until one or both become clearer, investors should expect more of the same—periodic pullbacks followed by cautious recoveries.