US stock futures traded in a narrow range Tuesday morning as investors adopted a cautious stance ahead of key inflation data and the start of earnings season from the country's largest banks. The muted open comes as oil prices climbed to a four-week high, adding to uncertainty about the path of interest rates.

What's Driving the Market

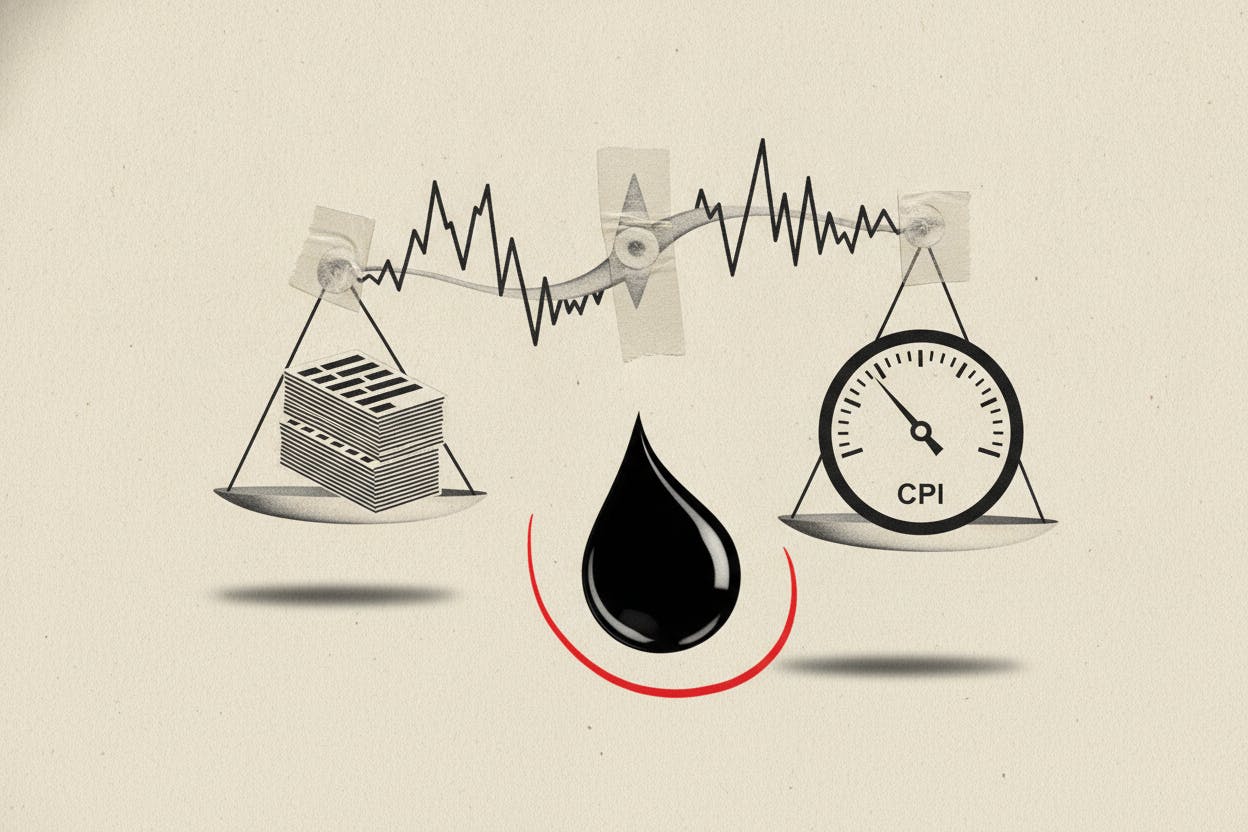

All eyes are on the June Consumer Price Index (CPI) report, due out later this week. CPI measures the change in prices paid by consumers for goods and services and is the most closely watched inflation gauge by the Federal Reserve. A hotter-than-expected reading could reinforce the case for another rate hike, while a cooler number might ease those fears.

Traders have already increased their bets on a July rate increase, according to fed funds futures data. The probability of a quarter-point hike at the Fed's next meeting has risen in recent days, partly due to the run-up in oil prices, which can feed into broader inflation.

Oil at a Four-Week High

Crude oil prices have been on the rise, hitting their highest level in about a month. The rally is driven by supply concerns, including production cuts from major exporters and geopolitical tensions. Higher energy costs can ripple through the economy, raising transportation and manufacturing expenses, which ultimately hit consumers' wallets.

For investors, rising oil prices often mean higher costs for airlines, shipping companies, and other fuel-intensive industries. At the same time, energy stocks tend to benefit from the price increase, creating a mixed picture for the broader market.

Big Bank Earnings on Deck

This week also marks the unofficial start of second-quarter earnings season, with several of the largest US banks set to report results. JPMorgan Chase, the country's biggest bank by assets, leads the pack. Its earnings are seen as a bellwether for the health of the financial sector and the broader economy.

Analysts will be watching for updates on net interest income—the difference between what banks earn on loans and pay on deposits—as well as loan demand and credit quality. The AI infrastructure boom has been driving steady deal flow for Wall Street banks, which could boost investment banking fees. However, higher interest rates have also made borrowing more expensive, potentially slowing loan growth.

Other major banks reporting this week include Citigroup and Wells Fargo. Citi recently posted its best quarterly revenue in a decade, thanks to volatile markets that boosted trading and deal fees. Investors will be looking to see if that momentum continues.

What It Means for Investors

The combination of inflation data, rising oil prices, and bank earnings creates a high-stakes environment for markets. If CPI comes in lower than expected, it could revive hopes that the Fed will cut rates later this year, potentially boosting stocks. On the other hand, a hot inflation print could push the Fed to hike again, which would likely pressure equities.

For everyday investors, the key takeaway is that markets are in a wait-and-see mode. The next few days could set the tone for the rest of the summer. It's a reminder that inflation and interest rates remain the dominant forces driving market direction.

Historically, periods of uncertainty like this can lead to increased volatility. Investors may want to review their portfolios to ensure they are diversified and aligned with their long-term goals, rather than making impulsive moves based on short-term data.

Looking Ahead

Beyond this week, markets will continue to parse economic data and corporate earnings for clues about the health of the economy. The Fed has signaled it will remain data-dependent, meaning each inflation report and jobs number will be scrutinized for signs of a slowdown or persistent price pressures.

For now, the message from the markets is clear: caution prevails. With oil at a four-week high and rate hike odds rising, investors are bracing for potential turbulence ahead.